34 ISE Magazine | www.iise.org/ISEmagazine

Consumer packaged goods (CPG) are purchased

items that consumers need to replenish frequently,

such as beverages, packaged foods and household

products.

With estimated 2017 sales of nearly $800 billion

contributing around 4 percent of U.S. gross domestic

product, these purchases play a critical role in the economy.

The industry is characterized by consumers’ low switch-

ing costs. For many years, a few giant players, such as Nestlé,

Procter & Gamble Co. and Unilever, dominated the industry

through product differentiation, market segmentation strate-

gies and brand loyalty.

Before 1930, consumer goods were sold in small neighbor-

hood general stores that satisfied local buyers’ needs. Packaging

and marketing did not play an important role in bulk deliveries

as households bought items daily from these small stores. The

first direct-to-consumer approach appeared at the beginning of

the 20th century when manufacturers such as Avon began sell-

ing beauty products door to door with housewives as the tar-

geted customers. Door-to-door selling techniques experienced

a rapid decline after 1980 when women joined the workforce

in larger numbers.

By 1950, big CPG manufacturers such as P&G and Unile-

ver, forced by better quality in competitors’ products, started

C

Direct-to-consumer strategies

for CPG manufacturers

Brick-and-mortar options give way to personalized services for a variety of goods

By Gurram Gopal and Inés de Madariaga Azcuénaga

Direct-to-consumer strategies

for CPG manufacturers

Brick-and-mortar options give way to personalized services for a variety of goods

By Gurram Gopal and Inés de Madariaga Azcuénaga

Direct-to-consumer strategies

for CPG manufacturers

Brick-and-mortar options give way to personalized services for a variety of goods

By Gurram Gopal and Inés de Madariaga Azcuénaga

Direct-to-consumer strategies

for CPG manufacturers

Brick-and-mortar options give way to personalized services for a variety of goods

By Gurram Gopal and Inés de Madariaga Azcuénaga

January 2019 | ISE Magazine 35

to invest in brand management. Companies started to take ad-

vantage of brand equity and use it to add long-term value and

justify charging more for their products. Increased spending on

marketing to drive brand equity became the key strategy for

CPG manufacturers.

In the 1990s, modern retail stores such as supermarkets in-

corporated pioneering marketing and management techniques.

Big retailers started to invest in marketing and to offer generic

products, and thus increased their reputation. Until now, CPG

manufacturers’ strategy had been based on three main aspects:

gaining tactical placement at the retailers’ shelves, brand posi-

tioning and mass advertising.

In recent years, the CPG industry has struggled to sustain

growth with sales flat between 2013 and 2016. Large manu-

facturers have focused on cost-cutting and trimming brands

while seeking new avenues for growth. The appearance of

e-commerce channels, the strengthening of powerful retail-

ers and changing customers’ needs and priorities inevitably led

CPG manufacturers to reconsider their strategy and adapt to

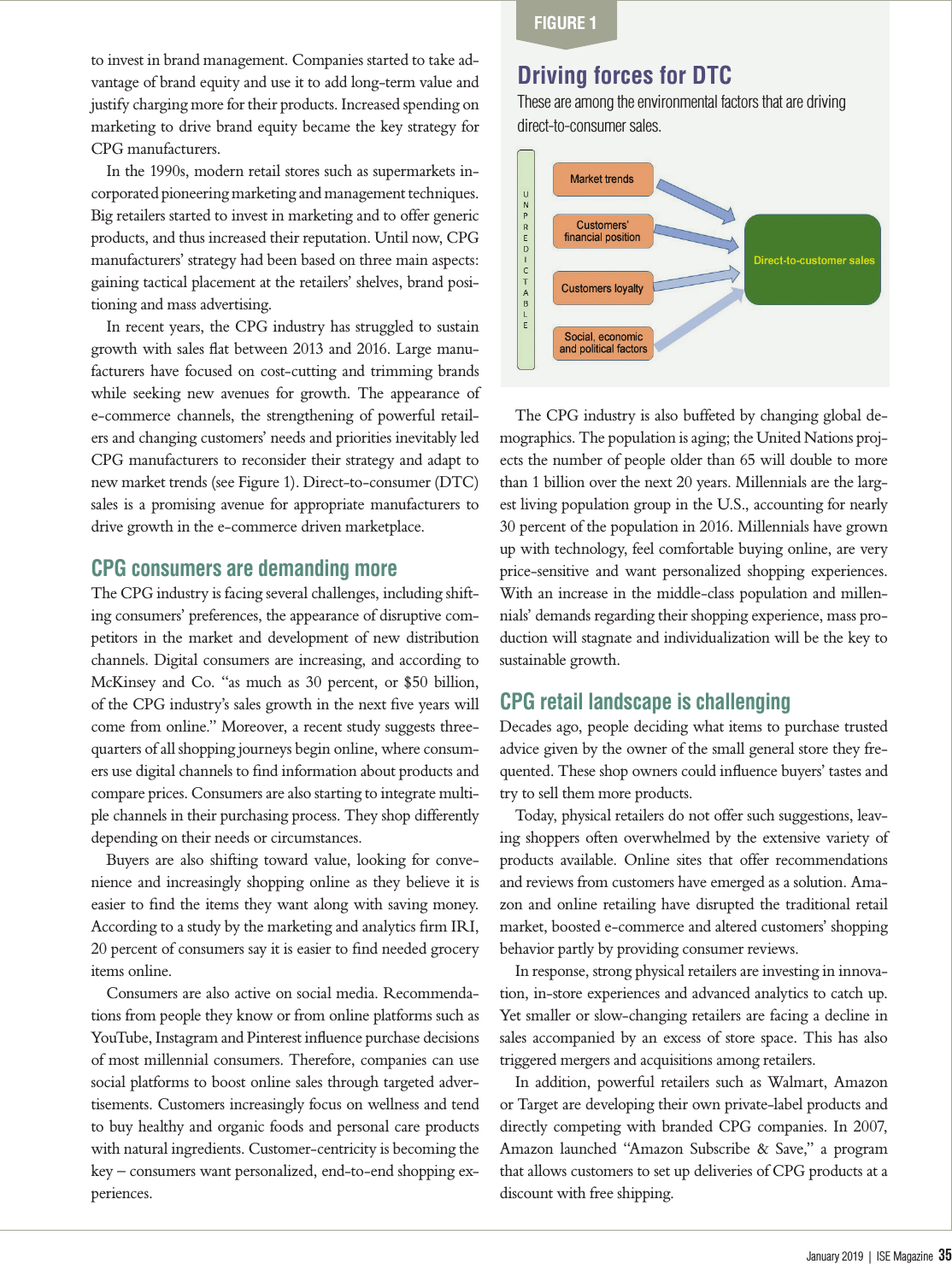

new market trends (see Figure 1). Direct-to-consumer (DTC)

sales is a promising avenue for appropriate manufacturers to

drive growth in the e-commerce driven marketplace.

CPG consumers are demanding more

The CPG industry is facing several challenges, including shift-

ing consumers’ preferences, the appearance of disruptive com-

petitors in the market and development of new distribution

channels. Digital consumers are increasing, and according to

McKinsey and Co. “as much as 30 percent, or $50 billion,

of the CPG industry’s sales growth in the next five years will

come from online.” Moreover, a recent study suggests three-

quarters of all shopping journeys begin online, where consum-

ers use digital channels to find information about products and

compare prices. Consumers are also starting to integrate multi-

ple channels in their purchasing process. They shop differently

depending on their needs or circumstances.

Buyers are also shifting toward value, looking for conve-

nience and increasingly shopping online as they believe it is

easier to find the items they want along with saving money.

According to a study by the marketing and analytics firm IRI,

20 percent of consumers say it is easier to find needed grocery

items online.

Consumers are also active on social media. Recommenda-

tions from people they know or from online platforms such as

YouTube, Instagram and Pinterest influence purchase decisions

of most millennial consumers. Therefore, companies can use

social platforms to boost online sales through targeted adver-

tisements. Customers increasingly focus on wellness and tend

to buy healthy and organic foods and personal care products

with natural ingredients. Customer-centricity is becoming the

key – consumers want personalized, end-to-end shopping ex-

periences.

The CPG industry is also buffeted by changing global de-

mographics. The population is aging; the United Nations proj-

ects the number of people older than 65 will double to more

than 1 billion over the next 20 years. Millennials are the larg-

est living population group in the U.S., accounting for nearly

30 percent of the population in 2016. Millennials have grown

up with technology, feel comfortable buying online, are very

price-sensitive and want personalized shopping experiences.

With an increase in the middle-class population and millen-

nials’ demands regarding their shopping experience, mass pro-

duction will stagnate and individualization will be the key to

sustainable growth.

CPG retail landscape is challenging

Decades ago, people deciding what items to purchase trusted

advice given by the owner of the small general store they fre-

quented. These shop owners could influence buyers’ tastes and

try to sell them more products.

Today, physical retailers do not offer such suggestions, leav-

ing shoppers often overwhelmed by the extensive variety of

products available. Online sites that offer recommendations

and reviews from customers have emerged as a solution. Ama-

zon and online retailing have disrupted the traditional retail

market, boosted e-commerce and altered customers’ shopping

behavior partly by providing consumer reviews.

In response, strong physical retailers are investing in innova-

tion, in-store experiences and advanced analytics to catch up.

Yet smaller or slow-changing retailers are facing a decline in

sales accompanied by an excess of store space. This has also

triggered mergers and acquisitions among retailers.

In addition, powerful retailers such as Walmart, Amazon

or Target are developing their own private-label products and

directly competing with branded CPG companies. In 2007,

Amazon launched “Amazon Subscribe & Save,” a program

that allows customers to set up deliveries of CPG products at a

discount with free shipping.

FIGURE 1

Driving forces for DTC

These are among the environmental factors that are driving

direct-to-consumer sales.

36 ISE Magazine | www.iise.org/ISEmagazine

Nimble companies offer

strong competition

There are many more products available in each cat-

egory than a decade ago, leading to a decrease in the

perception of brand value from which CPG manufac-

turers have benefited. This fact, along with the shorten-

ing of product life cycles, makes the need to adapt to the

new trends in customer demand a must to survive in the

CPG industry.

As the barriers to entry are increasingly lowered,

small competitors are taking advantage of e-commerce

channels and offering individualized shopping experi-

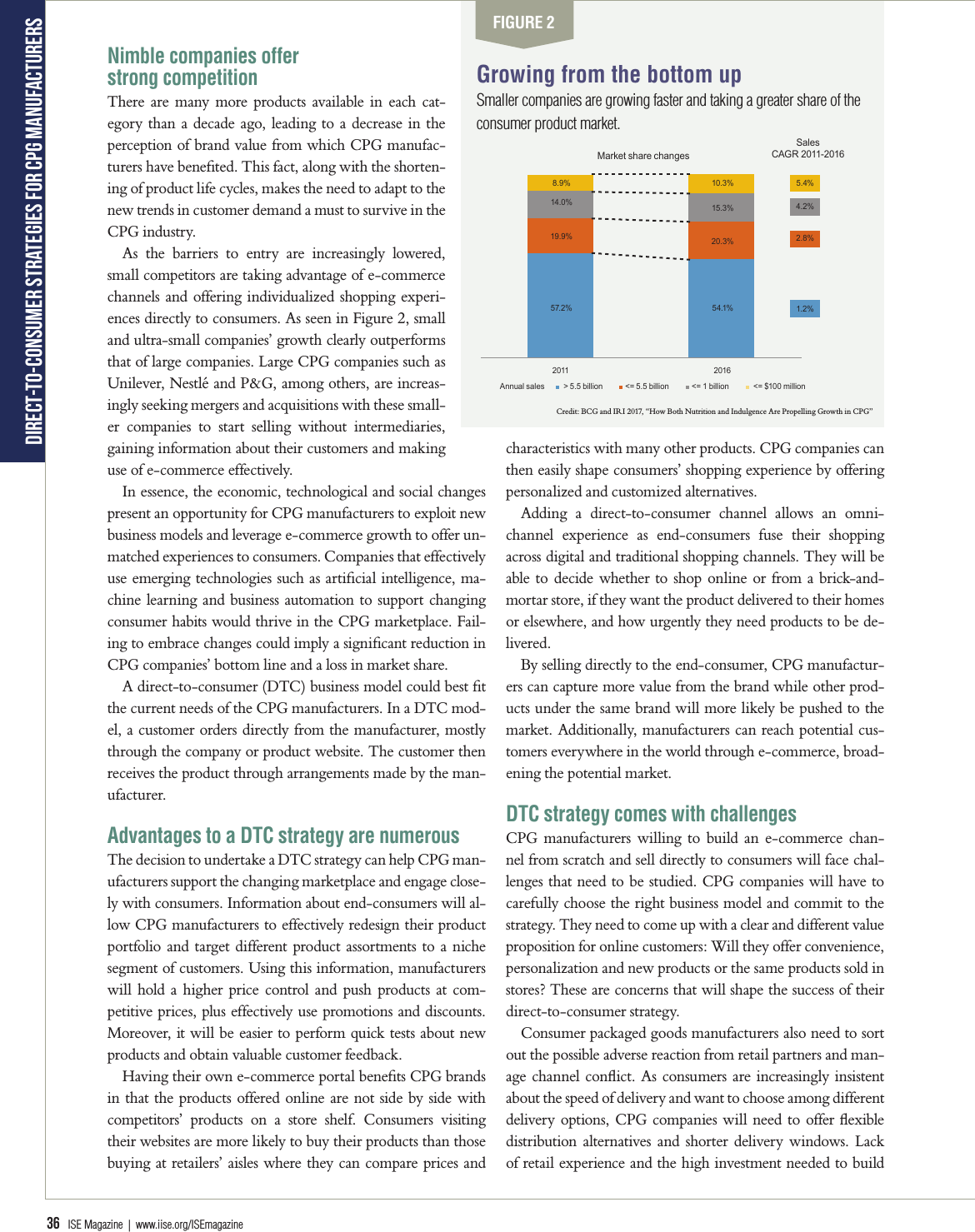

ences directly to consumers. As seen in Figure 2, small

and ultra-small companies’ growth clearly outperforms

that of large companies. Large CPG companies such as

Unilever, Nestlé and P&G, among others, are increas-

ingly seeking mergers and acquisitions with these small-

er companies to start selling without intermediaries,

gaining information about their customers and making

use of e-commerce effectively.

In essence, the economic, technological and social changes

present an opportunity for CPG manufacturers to exploit new

business models and leverage e-commerce growth to offer un-

matched experiences to consumers. Companies that effectively

use emerging technologies such as artificial intelligence, ma-

chine learning and business automation to support changing

consumer habits would thrive in the CPG marketplace. Fail-

ing to embrace changes could imply a significant reduction in

CPG companies’ bottom line and a loss in market share.

A direct-to-consumer (DTC) business model could best fit

the current needs of the CPG manufacturers. In a DTC mod-

el, a customer orders directly from the manufacturer, mostly

through the company or product website. The customer then

receives the product through arrangements made by the man-

ufacturer.

Advantages to a DTC strategy are numerous

The decision to undertake a DTC strategy can help CPG man-

ufacturers support the changing marketplace and engage close-

ly with consumers. Information about end-consumers will al-

low CPG manufacturers to effectively redesign their product

portfolio and target different product assortments to a niche

segment of customers. Using this information, manufacturers

will hold a higher price control and push products at com-

petitive prices, plus effectively use promotions and discounts.

Moreover, it will be easier to perform quick tests about new

products and obtain valuable customer feedback.

Having their own e-commerce portal benefits CPG brands

in that the products offered online are not side by side with

competitors’ products on a store shelf. Consumers visiting

their websites are more likely to buy their products than those

buying at retailers’ aisles where they can compare prices and

characteristics with many other products. CPG companies can

then easily shape consumers’ shopping experience by offering

personalized and customized alternatives.

Adding a direct-to-consumer channel allows an omni-

channel experience as end-consumers fuse their shopping

across digital and traditional shopping channels. They will be

able to decide whether to shop online or from a brick-and-

mortar store, if they want the product delivered to their homes

or elsewhere, and how urgently they need products to be de-

livered.

By selling directly to the end-consumer, CPG manufactur-

ers can capture more value from the brand while other prod-

ucts under the same brand will more likely be pushed to the

market. Additionally, manufacturers can reach potential cus-

tomers everywhere in the world through e-commerce, broad-

ening the potential market.

DTC strategy comes with challenges

CPG manufacturers willing to build an e-commerce chan-

nel from scratch and sell directly to consumers will face chal-

lenges that need to be studied. CPG companies will have to

carefully choose the right business model and commit to the

strategy. They need to come up with a clear and different value

proposition for online customers: Will they offer convenience,

personalization and new products or the same products sold in

stores? These are concerns that will shape the success of their

direct-to-consumer strategy.

Consumer packaged goods manufacturers also need to sort

out the possible adverse reaction from retail partners and man-

age channel conflict. As consumers are increasingly insistent

about the speed of delivery and want to choose among different

delivery options, CPG companies will need to offer flexible

distribution alternatives and shorter delivery windows. Lack

of retail experience and the high investment needed to build

FIGURE 2

Growing from the bottom up

Smaller companies are growing faster and taking a greater share of the

consumer product market.

Direct-to-consumer strategies for CPG manufacturers

Credit: BCG and IRI 2017, “How Both Nutrition and Indulgence Are Propelling Growth in CPG”

Sales

CAGR 2011-2016

Market share changes

8.9%

14.0%

19.9%

57. 2%

10.3%

15.3%

20.3%

54.1%

5.4%

4.2%

2.8%

1.2%

2011 2016

Annual sales > 5.5 billion <= 5.5 billion <= 1 billion <= $100 million

January 2019 | ISE Magazine 37

a digital channel might hamper the shift of some new CPG

companies toward a DTC strategy.

Finally, building a DTC channel entails an additional uncer-

tainty for management as illustrated by these examples.

Before Netflix, a person had to rent or buy a DVD

or videotape at a store to watch a movie at home. This

changed when Netflix started offering DVD rentals through

its website in 1998. Netflix evolved to revolutionize the en-

tertainment industry by introducing a subscription service

allowing anyone with an internet connection to stream the

latest movies and television shows to devices such as phones,

computers and TVs. It allows people

to schedule what they want to watch

and offers a wide variety of content in

multiple languages.

In 2013, Netflix decided to go di-

rect-to-consumer and started produc-

ing its own content to stay ahead of

competitors in a fast-changing indus-

try. Making its own shows and mov-

ies allows Netflix to avoid complex

international content arrangements

and differentiate itself from cable TV

providers. The company can retain

the rights to show its original con-

tent in nearly any country in perpe-

tuity. Its original shows, movies and

database of viewer preferences have

made Netflix the most successful on-

demand streaming service.

Harry’s launched in 2013 with

a subscription model to sell shav-

ing products directly to end-

consumers. Its products are simple

razors, but what it truly offers is an

easier shopping experience at low

prices. Customers will no longer run

out of cartridges nor have to go at the

last minute to a supermarket to buy

razors. Harry’s offers quality products

with free shipping, and replacement

blade cartridges are shipped automati-

cally based on customers’ shaving fre-

quency.

Harry’s has built a loyal customer

base by using social media effec-

tively. In the weeks before its launch,

it created a waiting list for potential

customers and rewarded people who

shared its campaign on social net-

works with free products (the more

referrals, the higher the prize earned).

The result: 100,000 people signed up on the waiting list in

only a week before even knowing what products Harry’s was

selling. This strategy allowed Harry’s to collect data from po-

tential customers and trigger the curiosity and engagement of

the marketplace. In 2016, Target partnered with Harry’s, and

in 2017 about 50 percent of Target’s razor handle sales and

about 15 percent of its cartridge sales came from Harry’s.

Along the same lines, Dollar Shave Club sells razors

and bathroom products through online subscription.

The company stands out by offering a wide range of prod-

ucts and monthly bundles. It has become a powerful brand in

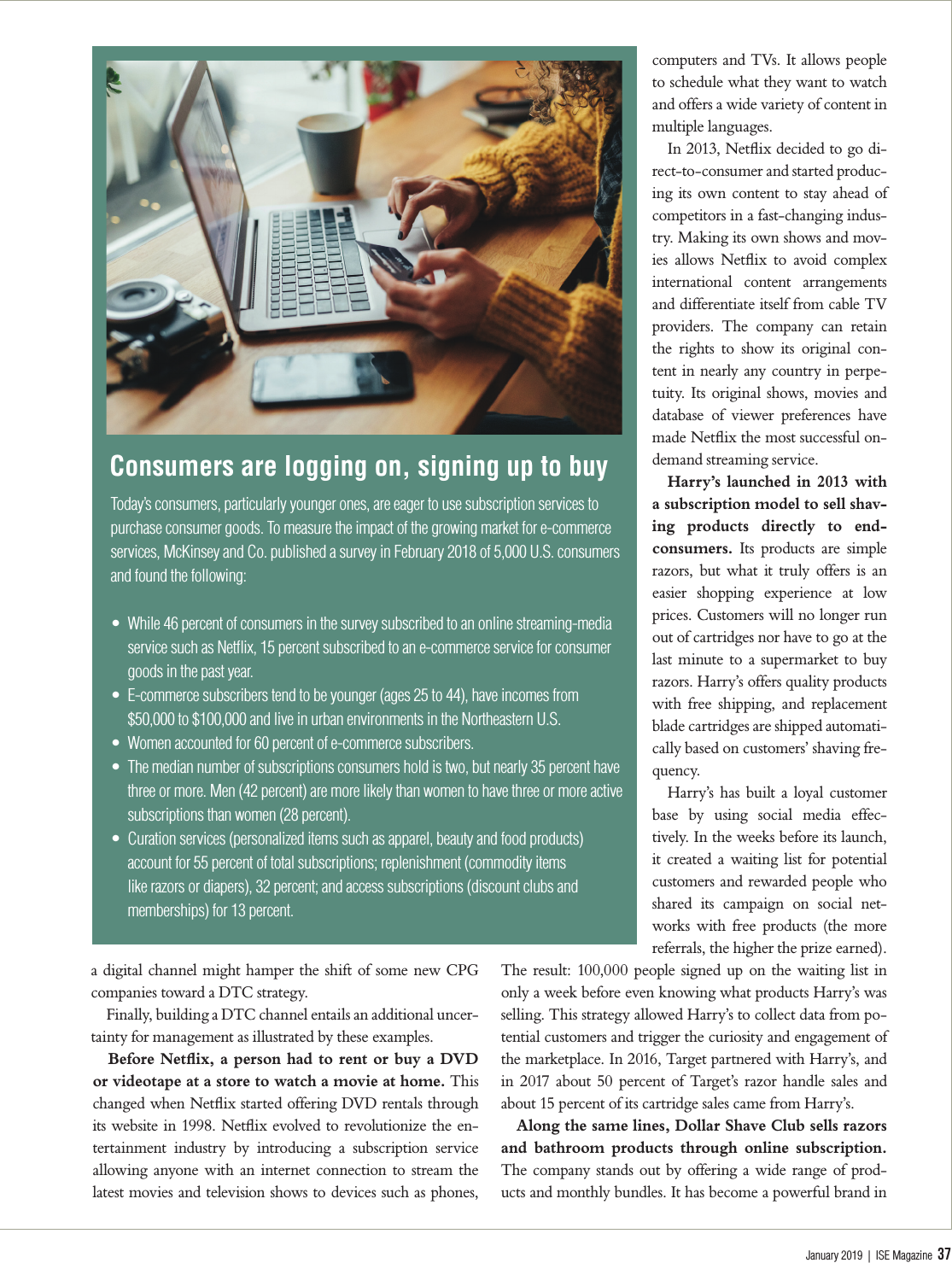

Today’s consumers, particularly younger ones, are eager to use subscription services to

purchase consumer goods. To measure the impact of the growing market for e-commerce

services, McKinsey and Co. published a survey in February 2018 of 5,000 U.S. consumers

and found the following:

• While 46 percent of consumers in the survey subscribed to an online streaming-media

service such as Netflix, 15 percent subscribed to an e-commerce service for consumer

goods in the past year.

• E-commerce subscribers tend to be younger (ages 25 to 44), have incomes from

$50,000 to $100,000 and live in urban environments in the Northeastern U.S.

• Women accounted for 60 percent of e-commerce subscribers.

• The median number of subscriptions consumers hold is two, but nearly 35 percent have

three or more. Men (42 percent) are more likely than women to have three or more active

subscriptions than women (28 percent).

• Curation services (personalized items such as apparel, beauty and food products)

account for 55 percent of total subscriptions; replenishment (commodity items

like razors or diapers), 32 percent; and access subscriptions (discount clubs and

memberships) for 13 percent.

Consumers are logging on, signing up to buy

38 ISE Magazine | www.iise.org/ISEmagazine

Direct-to-consumer strategies for CPG manufacturers

FIGURE 3

four years with a strong recurring revenue

model because of high customer reten-

tion. In 2016, Unilever acquired Dollar

Shave Club for $1 billion. That allowed

the CPG giant to compete with Gillette,

one of its biggest competitors and a P&G

razor brand, as well as to collect valuable

customers’ insights.

Bear Naked, now part of Kel-

logg’s, allows consumers to choose

from a variety of ingredients and

customize granola blends. The com-

pany’s products are made of whole grain,

have no artificial preservatives and are

vegetarian-friendly. Granola is not a fre-

quently consumed product, but through

offering different shopping experiences,

customization and following the market

trends of organic and healthy products, Bear Naked has expe-

rienced significant success.

Love Cocoa is a British company that sells hand-

made chocolate. It offers next-day delivery of fashionable

chocolate boxes that can be personalized and allows consumers

to subscribe to monthly deliveries.

Nespresso, by Nestlé, is a luxury coffee brand that

has an innovative business model focused on offering

high-quality coffee and building strong relationships

with consumers. Nespresso offers coffee machines tied to

single-serve capsules available at Nespresso. It sells directly to

consumers and has its own boutiques. Additionally, Nespresso

enhances consumers’ experiences with Nespresso Club and of-

fers multiple delivery options. It outsources production of the

coffee machines to third-party manufacturers to ensure profit

margins. The company uses targeted advertising and is present

in all major social networks. It has recently started an Insta-

gram influencer marketing campaign to reach other customer

segments.

P&G is offering DTC for Tide, its popular laundry

detergent, via Tide Wash Club. This service allowed sub-

scribers to have packets of Tide Pods delivered every two or

three months with free shipping. P&G selected Tide Pods, its

most expensive but popular laundry detergent, as the product

suitable for DTC because consumers would be willing to pay

more for convenient service.

Similarly, Ben & Jerry’s, owned by Unilever, recent-

ly let consumers purchase pints of ice cream directly

from its online site. It benefits from brand loyalty and charg-

es a premium for online products. Ice cream is not a frequently

purchased item, but Ben & Jerry’s has a loyal customer base and

it can offer a range of flavors. It does not have a subscription

service.

Nike is undertaking a substantial shift toward a di-

rect-to-consumer model that allows it to run a lean

business without significant inventory at retailers’

stores. Additionally, Nike tries to get closer to its customers’

lifestyles through different mobile apps. The company intro-

duced Nike Run Club, an app that allows fans to have person-

alized coaches, study their fitness level and compare it to that

of their friends. These apps allow Nike to gather a considerable

amount of information about their customers. Moreover, the

company offers shoe-customization through NikeiD that al-

lows customers to pick from a variety of “blank canvas” shoes

and decorate them with different colors. Another aspect that

has made Nike’s direct-to-consumer strategy successful is its

social media omnipresence.

VF Corp., parent company of Vans and The North

Face, among others, is another apparel and footwear

company that has built an e-commerce channel to cre-

ate stronger relationships with target consumers. Its

DTC channel accounts for 25 percent of its sales and accounts

for nearly 70 percent of the company’s sales growth.

Variables to DTC success

CPG covers a variety of product categories with their own

characteristics. Based on industry research and discussions with

managers of five CPG companies and two large retailers, we

identified a set of primary variables that play a key role in de-

termining the success of a DTC strategy. Frequency of usage is

a key factor in DTC as products that are used and replenished

more often can generate sustainable and predictable demand.

Product category growth rate in e-commerce is another

primary factor; categories that can benefit from price reduc-

tion when being sold online (razors, makeup, etc.) experience

strong growth. Personalization capacity, the ability to offer

personalized products that can create engagement and enhance

online shoppers’ experience, is the third primary variable.

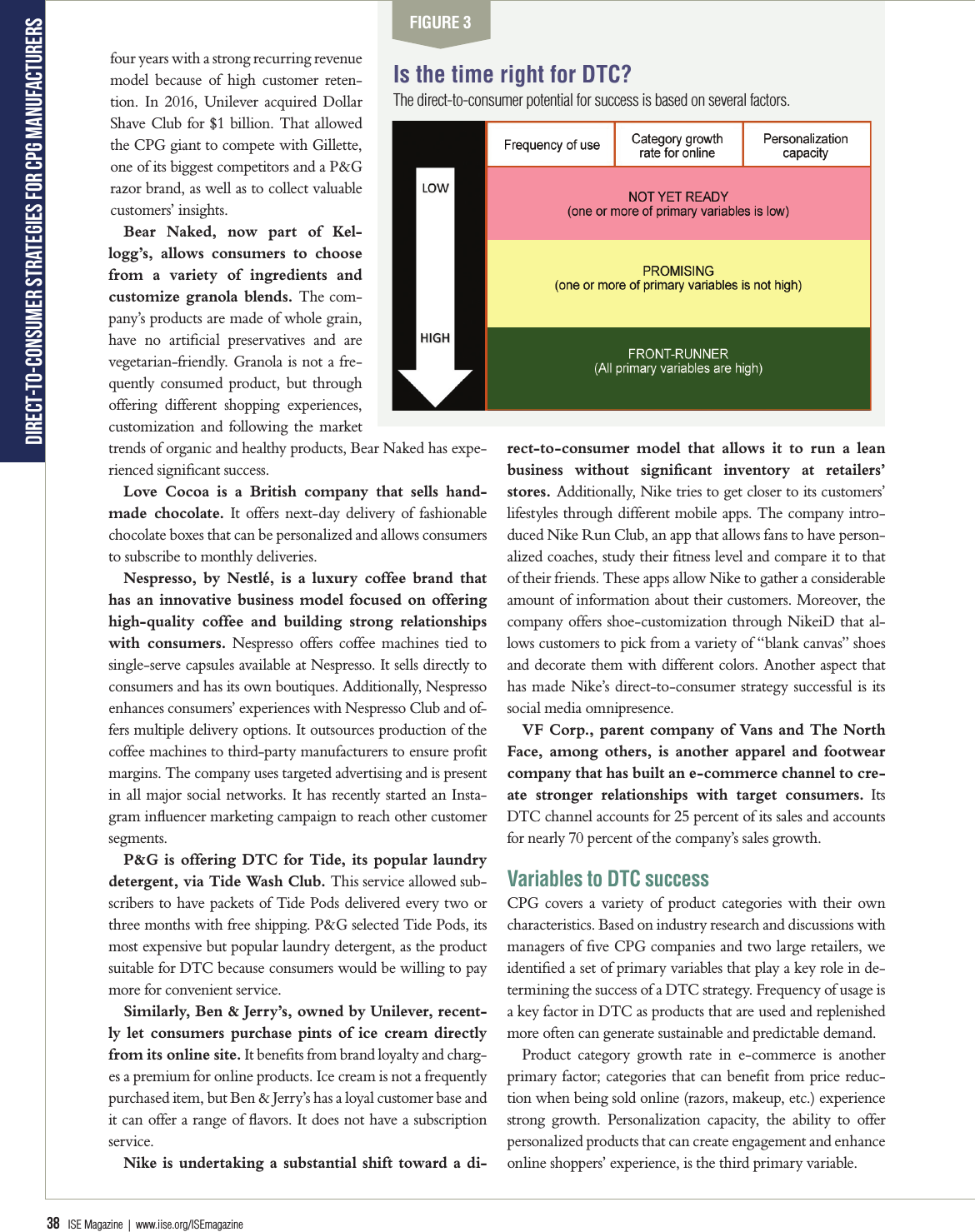

Is the time right for DTC?

The direct-to-consumer potential for success is based on several factors.

January 2019 | ISE Magazine 39

Depending on the values of the primary factors, CPG com-

panies can find themselves in one of the following groups (seen

in Figure 3):

• The “Not Yet Ready” group consists of companies that

have low scores for the primary variables required for a

DTC success and thus are not suitable for selling directly to

end-consumers currently.

• The “Promising” group are companies that meet the basic

requirements but need to improve on one or more variables

to reach the “front-runner” group. A company might sell

a frequently used product like toothpaste and might have

high online growth rates, but its ability to personalize might

be weak. Some companies might manage to improve and

move to the front-runner group while others might be

stuck in this group.

• The “Front-Runner” group: Companies that have high

values of the primary factors required to have a high prob-

ability of DTC success.

The ability to offer a subscription model is another impor-

tant factor in DTC implementation. A company can offer a

subscription of a fixed quantity and fixed price per replenish-

ment or charge a fixed price every period and let consum-

ers decide the quantity to be purchased in each period with a

yearly limit.

Managing last-mile logistics

Choosing the most effective way of transportation for the last-

mile delivery will be a complex issue for CPG companies, as

they must balance costs and delivery speed. CPG manufactur-

ers willing to sell food and perishable goods online must be

able to deliver products within hours, an additional challenge.

Figure 4 suggests some suitable transportation alternatives for

urban or rural areas, depending on the delivery speed required.

As for storage, a suitable alternative could be to use existing

startups such as Darkstore that use excess capacity in ware-

houses, malls and other storage facili-

ties as fulfillment centers. These cen-

ters allow brands to store inventory

in major cities to provide on-demand

delivery at low costs. Additionally,

these startups can partner with de-

livery companies and offer the whole

fulfillment service.

Have an effective

marketing strategy

CPG manufacturers must leverage

social media campaigns to gather

insights on potential consumers and

create engagement before launching

products. Later, companies should continuously collect con-

sumers’ data and use advanced analytics to direct marketing

efforts to the right consumer groups and change their offerings

according to consumer’s preferences. Companies will have to

devote significant marketing resources to drive DTC success

via customer acquisition efforts. This could include creating

mobile apps that augment the value of their products and con-

nect consumers.

The consumer-packaged goods industry is changing rap-

idly. Consumers have increasingly high expectations of con-

venience and personalization, retailers are consolidating

and startups are disrupting the traditional marketplace. The

framework proposed in this article highlights the critical fac-

tors needed to undertake a direct-to-consumer approach. A

successful DTC effort not only drives growth but also gives

manufacturers valuable end-consumers’ information, which

can provide the ultimate competitive advantage.

Gurram Gopal is an industry professor in industrial technology and

management at Illinois Institute of Technology with an interest in

industrial engineering applications. He has published more than 50

papers and articles and has presented extensively at academic confer-

ences. He received a 2011-2012 Fulbright Scholar Award to teach and

conduct research at Galway Mayo Institute of Technology in Ireland

and has been a Fulbright specialist candidate since 2013. Gopal devel-

oped marketing strategies for some of the world’s largest pharmaceutical

companies as a strategy consultant and manager for ZS Associates and

worked in strategic marketing, supply chain management and strategic

quality at Tellabs Inc. Along with certificates in ISO, CMM and

applied statistics and forecasting, Gopal holds a B.S. in chemical engi-

neering from the Indian Institute of Technology, Madras, and an M.S.

and a Ph.D. in industrial engineering from Northwestern University.

Inés de Madariaga Azcuénaga is a strategy consultant. She holds a

master’s in industrial engineering from UPV/EHU in Spain and a

master’s in industrial technology and operations from Illinois Institute

of Technology.

FIGURE 4

Last-mile logistics: Delivering the goods

Here are transportation options available for direct-to-consumer goods based on urgency

of delivery and customer expectations.